Why my family joined CrowdHealth.

I used to believe health insurance was a necessary evil. Another mandatory part of adulthood, it was right up there with paying taxes and showing up for jury duty.

Especially with three little kids in the picture—whose favorite pastimes include collecting germs, climbing tall trees, and face-planting off of furniture. As any parent reading this can imagine, opting out of traditional insurance felt not only irresponsible, but financially reckless. Like we were just begging for something horrible to happen.

Believing we had no other choice, we begrudgingly accepted the status quo.

But as the years went on, my frustration with the healthcare system continued to grow. We never knew what services were going to be covered and what wasn’t, and we hated that our choice of medical providers was limited based on whether they were “in network.”

ENTER CROWDHEALTH

Everything came to a head this past March when Scott started a new job. For the first time in five years, we had a clean break and the chance to try something different. But we didn’t walk away without a plan. After months of comparison charts, Reddit rabbit holes, and spreadsheet math, we landed on something that—if it worked the way it claimed to—felt like a real solution.

It’s called CrowdHealth, and it’s a peer-to-peer crowdfunding platform designed for people who prioritize their health. Just a couple months in, we’re already wondering why we didn’t make the switch sooner.

Sidebar: While I do enjoy talking about the things that make my life better, I rarely dedicate an entire blog post to a specific product or service. (My free time is precious to me, and I don’t find writing product reviews particularly riveting.) That’s how you know what I’m sharing today is special. This post is not sponsored, but the link provided is a referral link, which means we both benefit financially when you use it to sign up. As always, thank you.

Taken during an afternoon at BarnHill Vineyards in Anna, TX with friends.

I’m going to list the main reasons we love it, plain and simple—not because I’m trying to sell you, but because a post like this would have saved me a ton of time and research when I was shopping around for insurance alternatives a year ago. It hits different hearing it straight from another mom, ya know? Hopefully this comprehensive review provides some clarity on what CrowdHealth is, how it works, and why it’s worth your consideration.

→ It saves us money.

Let’s start with what everyone cares about most: the impact on your bank account. My biggest concern before joining CrowdHealth was whether it would actually end up being more cost-effective than traditional insurance. I’m happy to report that, for us, it absolutely has been.

Each month, there are two parts to what we pay: The first is the membership (or “advocacy”) fee, which is $60 per person. As a family of five, that comes out to $300 a month—less than half of what our insurance company charged.

The second piece is our portion of the group’s medical needs. For us, that’s $420 per month maximum, depending on what’s happening across the community. In other words, the absolute most we will spend on CrowdHealth in one month is $720. So far, though, we’ve not had to pay the full amount; in April, for example, our total cost (advocacy fee + crowdfunding contribution) was only $499.

Sidebar: That’s for a family of five. For single people under the age of 55, total fees are capped at $200/month.

I think it’s worth mentioning that Scott’s company paid for most of our insurance fees, and we still walked away—for all of the reasons listed below. (No regrets.) But if you’re self-employed and/or paying for your own insurance, CrowdHealth is a no-brainer. Here’s why:

1. You’re not paying costly premiums for high-deductible plans.

With traditional insurance, lower monthly premiums usually mean higher deductibles.

That’s what we had.

We were partnering with Scott’s place of employment to pay $650/month for a high-deductible plan. But the first $3,300 of in-network expenses—per person, or $6,600 for our family—was on us, before insurance would meaningfully contribute to anything.

And even after meeting that deductible, we were responsible for a 10-20% coinsurance until we reached our maximum out-of-pocket costs, which totaled $6,400 per individual (or $12,200 for the family).

Healthcare in the United States is an unbelievably expensive system, even for people who technically “have insurance.” Is it any wonder why 200,000 American insured families go bankrupt every year as a result of medical debt?

With CrowdHealth, members are only responsible for the first $500 of any eligible health event before the community helps fund the rest.

A “health event” is essentially any unique medical issue requiring care that exceeds $500—things like pregnancies, ER visits, surgeries, injuries, or chronic illnesses. Follow-up appointments, prescriptions, labs, and testing tied to the same issue are generally grouped together under that single event.

2. Self-pay prices are often dramatically cheaper.

This was one of the most surprising things we learned.

When you remove insurance from the equation and simply ask providers for their cash-pay pricing upfront, the prices are often significantly lower.

And honestly, it makes sense.

Healthcare pricing in this country is bizarrely opaque because providers and insurance companies negotiate rates behind closed doors. Patients rarely know what something actually costs until weeks later when a bill randomly shows up in the mail. Can you think of another industry that operates that way?

Not to mention, paying your doctor directly eliminates the need for middlemen, ensuring that you get to call the shots on your own care.

3. CrowdHealth negotiates on our behalf for the best price.

One thing that gave us peace of mind is that CrowdHealth also helps negotiate larger medical bills directly, often reducing costs by 30-60% for planned procedures and up to 90% for emergencies.

So while you’re more involved in the process overall, you’re not completely on your own trying to navigate everything yourself. Simply contact your Care Advocate (more on this later!) before a scheduled procedure to shop around or right after receiving a large emergency bill to get the price down.

I’ll also say this: One hesitation we initially had about switching was losing access to our HSA.

Since CrowdHealth is not an HSA-qualified health plan, you can’t continue making new pre-tax contributions. However, if you already have money sitting in an HSA, you don’t lose it. You can still use those existing funds toward eligible medical expenses—including the $500 member responsibility per health event.

→ Your contribution goes toward helping real people, not a mega corporation’s bottom line.

At its core, CrowdHealth is built around a simple idea: Instead of paying into a giant insurance corporation, you’re part of a community that supports each other’s medical needs.

This is where the whole thing clicked for me.

I genuinely like knowing where our money is going each month. It feels far more relational and trustworthy than blindly paying premiums into an industry that profits when claims are denied.

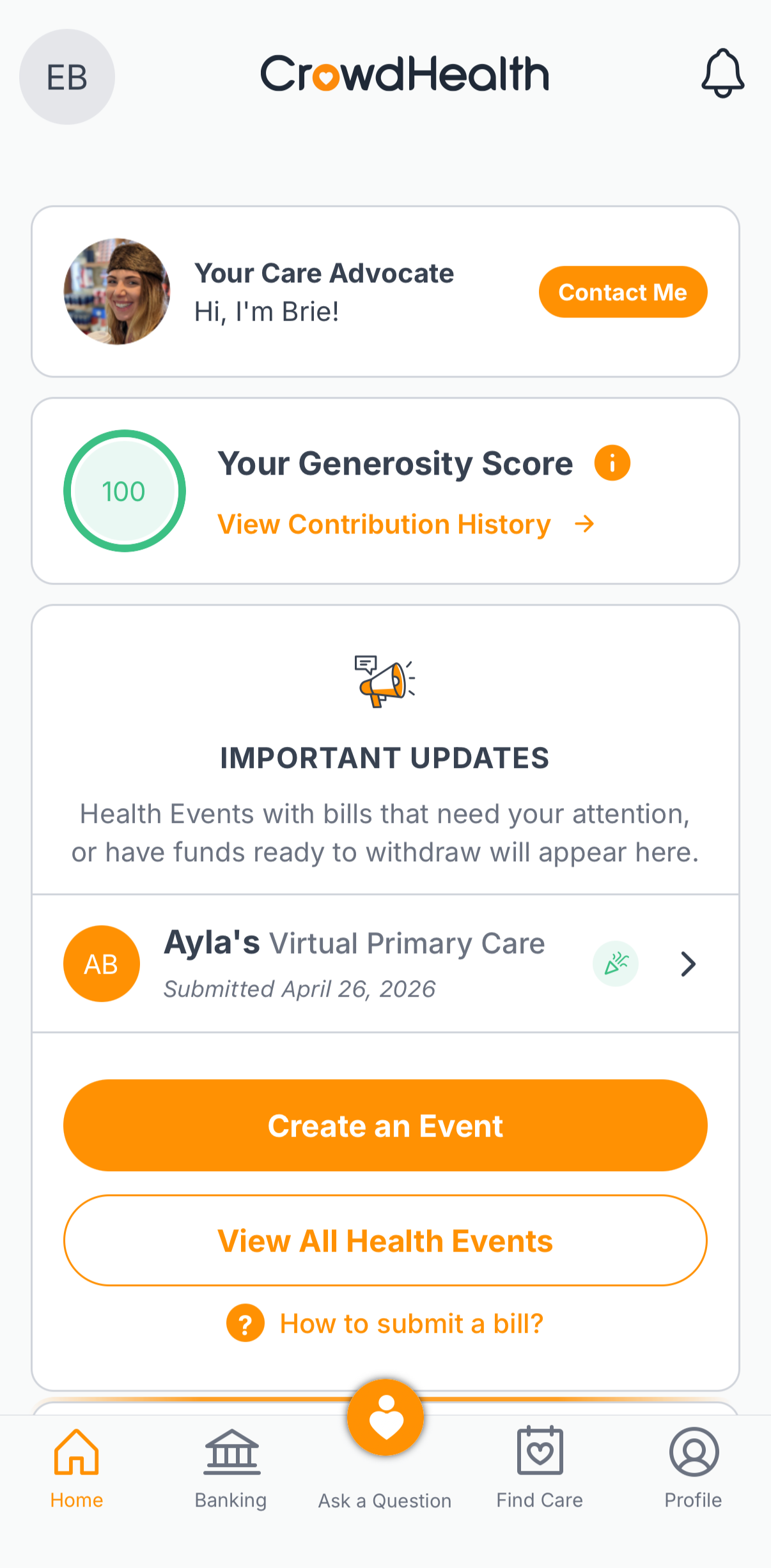

As a member of CrowdHealth, you’re incentivized to give. Every member has what’s called a Generosity Score, which reflects how consistently they contribute. The system is designed to reward participation and discourage people from simply taking from the group without paying it forward.

According to CrowdHealth, 99.9% of submitted bills have been successfully funded by the community. The remaining tiny fraction largely came from members with consistently poor Generosity Scores who repeatedly denied requests.

It functions well because it’s based on the mutual benefit principle: You pick someone up when they’re down, and they’ll do the same for you.

And unlike traditional insurance companies—which often profit by paying out as little as possible—the incentive here is the exact opposite: The whole community succeeds when the one is supported.

→ Routine visits are handled. And so are the worst-case scenarios.

I’m sure you can guess the question everyone immediately asks when I tell them we don’t have health insurance: “What happens if there’s a catastrophe?”

Trust me—we asked the same thing.

A major accident. Emergency surgery. Cancer. A long hospitalization. Those were the scenarios we thought through carefully before making the switch. And to be clear, we would not have joined if we weren’t confident that those kinds of situations could realistically be funded through the platform.

One CrowdHealth member accidentally shot himself on a solo fishing trip in Montana. The bullet went through his calf, thigh, and chest, requiring him to be airlifted to a hospital and placed in a coma. CrowdHealth negotiated his $1 million medical bill down to less than $250,000, and all of it was funded by the community.

If major illnesses are what concern you most (me too!), know this: There are somewhere between two and three dozen people with cancer using CrowdHealth, and the thousands of dollars worth of imaging, labs, procedures, and treatments are being taken care of.

But worst-case scenarios aren’t the only area in which CrowdHealth shines.

Pregnancy was a huge consideration for us. We’re not sure if we’re done having kids, and I didn’t want the deciding factor to be that we didn’t have health insurance.

During the years I was pregnant, we hit our deductible every single time. Each pregnancy cost us more than $6,000 out of pocket, and these were uncomplicated, low-intervention births. No epidurals. No emergencies. No major interventions. Just standard OB care and hospital fees.

Not only is pregnancy eligible for funding, but babies are CrowdHealth’s #1 expense. (I mean, incredible.) The only rule is that you must be a member for at least 300 days before the estimated due date. (So if you joined today, you would need to conceive after June 10 in order for the pregnancy to be eligible.) The wonderful news? Pregnancy-related expenses are treated as a single health event, meaning the total member responsibility is capped at $3,000 for the entire pregnancy, birth, and postpartum care combined.

Compared to what we previously paid through traditional insurance, that difference alone was enough to get our attention.

What I personally love is the flexibility it creates. You’re not boxed into a narrow provider network or forced into one specific model of care. Whether that means working with a midwife, choosing a birth center or home birth, or simply having more autonomy over your healthcare decisions, it opens up options that traditional insurance often limits. That freedom feels a lot more aligned with how I think healthcare should work in the first place.

Fun fact: Half of all CrowdHealth babies were born at home in 2025.

It doesn’t stop there, though. As parents, we spend a decent amount of time at pediatricians’ offices. Routine visits add up quickly, especially during the early years. Under CrowdHealth, related appointments (similarly to pregnancy) can be grouped together under a single health event. For example, Max’s well-child visits are considered one health event until he’s three. Once we meet the initial $500 member responsibility for that event, additional eligible costs tied to it can be submitted for crowdfunding.

→ The app is beautifully designed and extremely user-friendly.

I’m not tech-savvy, so simplicity within the app was a must.

There’s also lots of hand-holding for beginners. Upon registering, you’re immediately paired with a human Care Advocate who is always available to answer any questions and concerns via direct messaging in the app. (I’ve reached out to ours, Bree, on several occasions, and it’s never taken her more than 24 hours to respond. Talk about a very different experience than trying to connect with an insurance company representative. #IYKYK)

CrowdHealth is not insurance, so there is a bit of a learning curve involved if “pay-it-and-forget-it” is what you’re used to. But if I can do it, so can you.

The process, from start to finish, is a breeze: At every medical appointment, we simply ask for cash-pay pricing, pay upfront, and then submit the bill through the app as a health event. From there, CrowdHealth reviews it, and it gets shared with the community for funding.

You’ll be notified quickly whether your funding request gets a green or red light. If it’s green, you’re good to go. (Requests get flagged red if the bill is 20% higher than fair market rates, or if the member has a Generosity Score below 90%.)

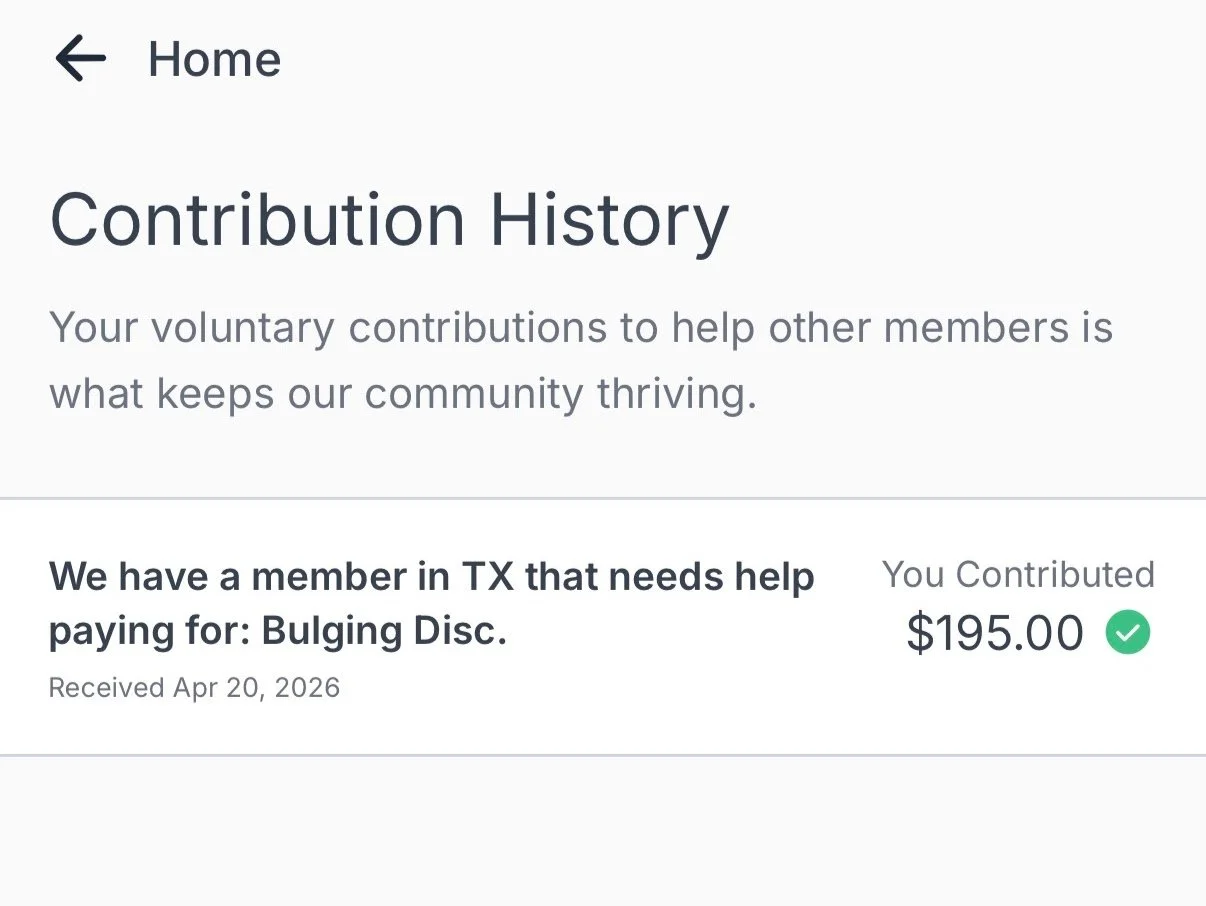

On the giving side, you’ll be notified once monthly via the app or email about contributing to someone else’s medical bills. (Don’t worry, you’ll never be bombarded with multiple requests in a single month.) We have ours set to automatically approve each request, so that I don’t waste any time approving it manually. This month, I was informed that we gave $195 to someone treating a bulging disc.

→ You get to choose your own doctor.

No provider directories. No worrying about staying “in network.” No realizing after the fact that your lab work was apparently sent to the wrong facility and is now being billed differently.

You simply choose the providers you trust, whether that’s a regular MD, chiropractor, functional medicine doctor, or naturopath. As long as your treatment plan falls under a specific health event, it doesn’t matter who treats you. (Curious about maintenance care? See below!)

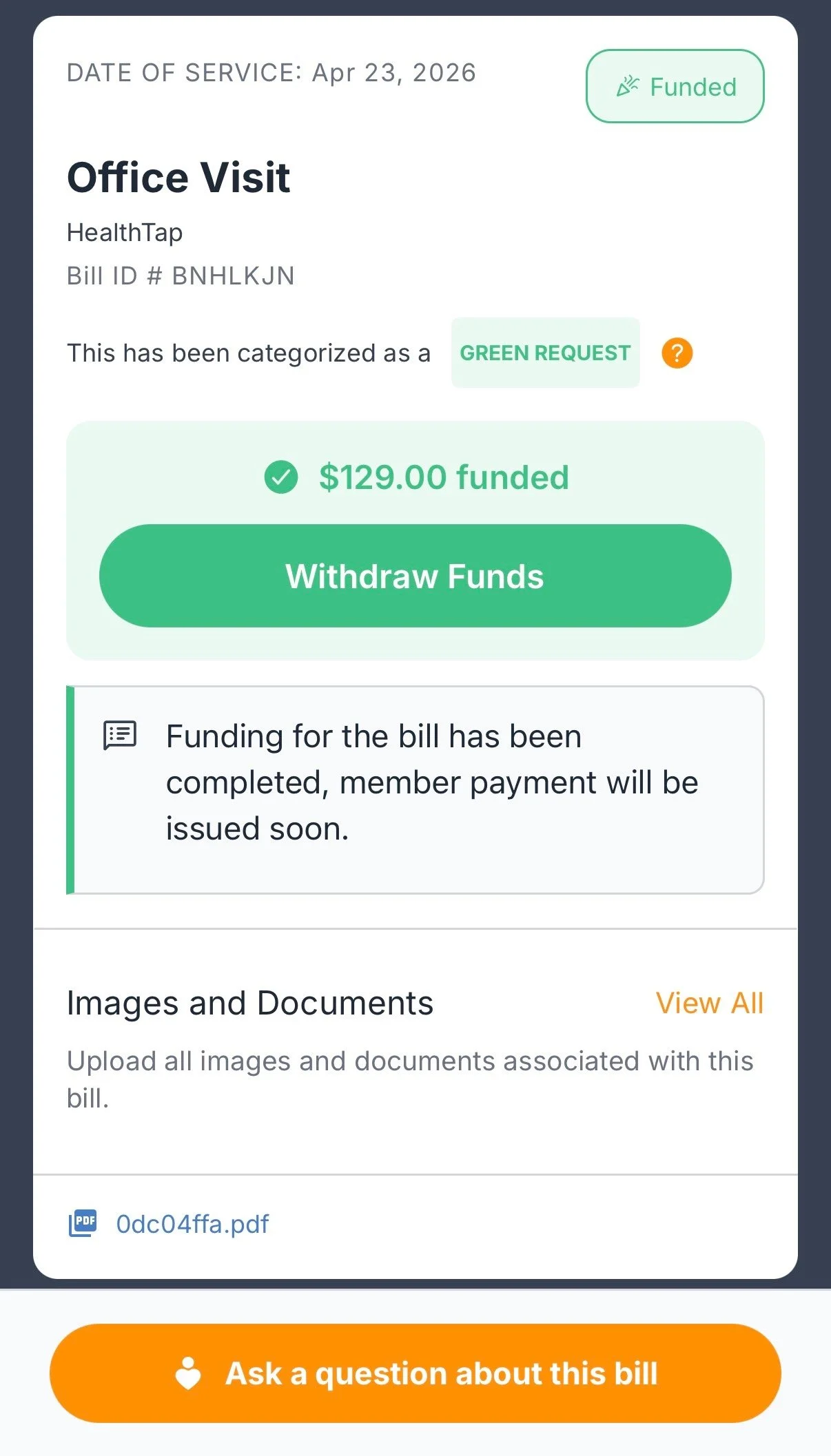

For the small stuff, CrowdHealth offers reimbursable virtual primary care through HealthTap. We’ve already had to make one telehealth appointment for poor Ayla, who came down with a stomach bug in late April. Lucky for us, the visit was refunded within a week. (And the Zofran her doctor prescribed was a life-saver.)

If you need some direction for a specific illness or injury, CrowdHealth’s doctor database has over 30,000 quality medical practitioners with affordable rates to choose from.

→ There are safeguards in place to protect the group.

Did you know that 70-90% of healthcare spending in the U.S. goes to treating chronic conditions—which are largely influenced by diet and lifestyle? I don’t know about you, but I don’t really want to pay for the medical expenses of someone who smokes a pack a day and eats Oreos for breakfast.

That said, there are some eligibility requirements in place that serve to protect the Crowd as a whole from unfair requests. We found them to be perfectly reasonable.

1. You have to be younger than 65 years of age, mostly because it conflicts with Medicare laws.

2. You have to be a non-smoker (for at least a year).

3. Men must weigh under 260 pounds, and women less than 220 pounds.

4. Certain states with an individual MEC mandate (e.g., California, District of Columbia, Massachusetts, New Jersey, Rhode Island, Vermont) require ACA-compliant insurance.

5. Pre-existing or previously diagnosed conditions are not eligible for crowdfunding in the first or second year of membership.

This kind of model only works if the community as a whole is relatively healthy, and I think it’s safe to say this won’t be the right fit for everyone. If you have significant ongoing medical needs that require consistent, predictable coverage, CrowdHealth could feel stressful instead of freeing.

→ Preventative health is highly encouraged.

This might be my favorite part of CrowdHealth.

Unlike traditional insurance—which was structured to support our current “sick care” system by largely engaging with people only after they’re already unwell—CrowdHealth actually incentivizes preventative health practices.

As a Nutritional Therapy Practitioner, I deeply believe in the value of integrative medicine—and I don’t mind investing money into the kinds of routine testing and therapies that help me feel my best and optimize my health for the long haul. While CrowdHealth’s guidelines exclude complementary wellness or maintenance care (e.g., nutrition coaching, acupuncture, etc.), members are able to bypass the usual $500 member responsibility once per year for any preventative exam performed by a licensed or board-certified practitioner, up to $300. I plan to use this extra money for my annual lab work.

CrowdHealth also partners with BetterHelp for free talk therapy, and showcases a different wellness company every quarter by offering discounts on specialized testing. This month, Scott completed a heavily discounted TinyHealth Gut Microbiome Test as one of CrowdHealth’s quarterly specials.

Bonus perk: Members can earn up to 20% off their monthly fees by "passing" health screenings, such as for fasting insulin, CRP, or DEXA scans. How cool is that?

It’s one of the first healthcare models I’ve personally encountered that actually rewards people for trying to stay healthy.

SIGN UP ON YOUR OWN TERMS

If you’ve been feeling some of the same frustrations we were with traditional insurance, CrowdHealth could be a really good option to explore. There’s no enrollment period to abide by, so you could technically sign up today and cancel tomorrow if you wanted.

When you sign up using my discount code WITHCANDOR, your maximum monthly community contribution is reduced to $39 per member for your first three months. That brings your total monthly cost to about $99 per person during that time, which makes it a much easier entry point.

Again, this isn’t traditional insurance, which means that funding is never guaranteed. As with everything, I recommend doing your own research before registering.

FINAL THOUGHTS

At worst, the modern-day health insurance industry in the U.S. is the largest scam this country’s ever seen. At best, it’s a confusing and expensive hassle that doesn’t always deliver—not only for patients on the receiving end of care, but for the medical providers working tirelessly within a system that’s broken.

If you happen to enjoy the endless hold times, the complicated explanations of benefits, and the surprise bills that show up in your mailbox months later, CrowdHealth probably isn’t for you.

Living their best lives.

Switching away from traditional insurance felt like a big decision, but staying in something that consistently didn’t make sense was riskier. Joining CrowdHealth has made us more intentional. More informed. And honestly, more empowered in our healthcare decisions than ever. We’re no longer at the mercy of a system we didn’t fully understand.

This isn’t just about cost, although that’s certainly part of it. It’s about stepping into a model that actually aligns with how we think about health: prioritizing prevention, valuing transparency, and being part of something that feels more human and less transactional.

Needless to say, there are so many parts of traditional insurance that I don’t miss at all. That constant low-level friction is just…gone. CrowdHealth isn’t for everyone, but for our family, it’s been a really refreshing shift—one that I don’t see us going back from anytime soon.

Top photo by Jeremy Thomas.